Be fearful when others are greedy and greedy when others are fearful. – Warren Buffett

Well, that was some beginning to 2016! We knew that volatility was coming our way but we did not foresee what happened in Q1. The Dow Jones managed to complete a round trip ticket as we fell 13% and subsequently rose back up 13% in one quarter. That is the biggest intra quarter comeback since the middle of the Great Depression in 1933. Our portfolio strategy coming into 2016 was to tactically manage our asset allocations given that we expected higher volatility and lower returns. Although we didn’t see a round trip in the offing for Q1 of 2016 our strategy worked out quite well. We believe that the rest of 2016 has much the same in store as the market reacts to every nuance emanating from the Eccles Building in Washington DC which is the home of the Federal Reserve Bank of the United States.

We believe that risks are rising after our second 12% rally in months. We have elevated valuations and falling earnings estimates for US companies. It is going to be difficult for the stock market to move higher from here but we cannot bet against continued central bank largesse. The stock market, having rallied 13% off of its recent lows in early February reminds us of a blog post from back in October of 2015. This is what we had to say back in October.

October 2015 will go down as the best performing month for the S&P 500 in four years. I think that we all enjoyed the ride back up in October. The S&P 500 rallied 8.3% and followed through with more gains today to get the S&P 500 into the plus column for 2015. Those gains would be nice gains for an entire year – never mind a month! Whenever we get to thinking how much we have gained we cannot help but to contemplate the downside. We must always be on guard to temper our greed/ego just as much as we would concentrate on opportunity when fear strikes.

As a reminder, the volatility continued then as well. The S&P 500 closed October of 2015 at 2080. It would be 10% lower by January of 2016.

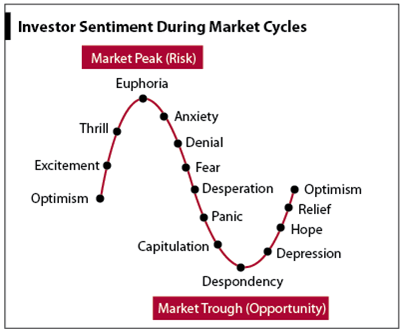

The key to making money in your portfolio lies in Investor Psychology. Understanding investor psychology and our own personal relationship with money is the key to successful investing. Having just ridden the roller coaster of emotions that was Q1 we are in a good position to replay how the highs and lows of the market made us feel and how we reacted to it. The two following charts can help you be more successful in understanding how emotions play a role in your investing process. The first shows two 12% rallies in the last 7 months. The second is a chart of investor psychology. After our second 12% rally in 7 months we should revisit how that roller coaster made us feel. Were you despondent at the lows? Did it make you want to sell and get out or buy more? Are you now relieved? Optimistic? Are you aching to buy more as prices rise?

In order to be on the right side of the market it is important to sell risk when prices are rising and buy risk when prices are falling. Or in emotional terms, when prices are falling and you are scared ask yourself “What should I be buying”? When prices are rising, ask, what are we selling? Understanding and keeping your emotions in check is the key to making money in markets like these. Ride the roller coaster.

Valuations

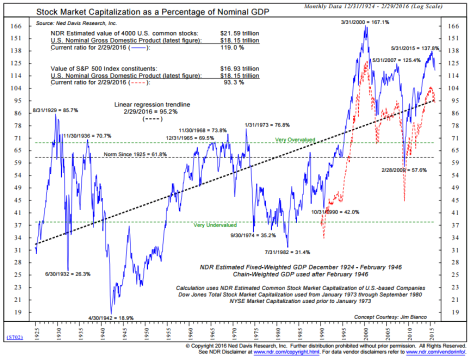

For long time readers and clients you know that one of our favorite metrics of stock market valuation is the US Stock Market Capitalization to GDP. It also happens to be Warren Buffett’s favorite metric in case you wonder why we follow it as well. As you can see from the following chart courtesy of Ned Davis Research the last time that the Stock Market Capitalization as a percentage of GDP was in an undervalued position was in July of 1982.

What changed since the early ’80’s? Central banks gained enormous influence over markets when President Richard Nixon took the United States off of the Gold Standard. This allowed central banks to help manage booms and busts in the economy without being hamstrung by the amount of gold in Fort Knox. Theoretically, they now had an unlimited supply of gold with printed fiat money taking the place of gold. This was the dawn of the Golden Age of Central Banking. The Prime Interest rate from the Federal Reserve reached its high of 21.5% in June of 1982. We have had a steady trend of lower interest rates for the last 30+ years.

Since 1995 (with the exception of February 2009) we have been in the overvalued area of the chart. This chart is evidence of the inexorable influence of central banks on asset prices. Some questions remain. Are we in a permanent state of overvaluation due to the influence of central bankers? If that state of overvaluation is not permanent at what point does central bank influence wane and valuations retreat to historical levels. Also, if central bankers remain in control of markets how low will central bankers allow markets to descend? Given our current inflated valuations we know that based on history we can expect lower returns over the next 10 year time frame.

Another natural question is posed if we feel that returns are to be muted or that prices should retreat. Why not sell out of all our assets and wait things out in cash? I think that the chart also answers that question. We have been in a perpetual state of overvaluation since 1995 – over twenty years! In order to meet our investing goals we cannot afford to sit out markets until they become more rationally priced. There is also the distinct possibility that markets become even more overpriced. If inflation were to take hold here in the United States investors would want tangible assets that rise in value with inflation. Equity prices could become wildly overpriced. John Maynard Keynes, the legendary economist once said, “markets can stay irrational longer than one can remain insolvent” betting against them.

We know that it has been a goal of central banks since the dawn of the crisis in 2008 to raise asset prices and therefore raise confidence in the economy but they are now distorting price discovery with monetary policy. This extreme action taken by central banks takes away some of our normal techniques for evaluating markets as markets are warped by policy.

Less Gas in the Tank

Unfortunately, the Federal Reserve has recently discovered with its latest interest rate hike that they are now the WORLD’s central bank and its moves have outsized effects on the rest of the world. Central banks can pull future returns forward and stall for time so that legislators can enact fiscal policy with which to mend an ailing economy. However, due to reluctance or ineptitude legislators have done nothing and left central banks, and in particular, the US Federal Reserve as the only game in town. If the Federal Reserve raises rates it then weakens other currencies and encourages capital flight. Capital goes where it is treated best. Higher rates of interest in the US and a stronger US Dollar force money to quickly flood out of emerging nations and into the United States. Central banks are stalling for time and currency wars are de rigueur. We have entered a “Twilight Zone” of monetary policy with negative interest rates in Europe and Japan. Central bank officials are also faced with the fact that monetary policy is not immune to the effects of the Law of Diminishing Returns as we enter Year 8 of a bull market in stocks.

Most likely, as risk premiums increase, central banks will increasingly ease via more negative interest rates and more QE, and these moves will have a beneficial effect. However, I also believe that QE will be less and less effective because there is less “gas in the tank.” – Ray Dalio Bridgewater Associates 2/18/16

What’s Next?

And while QE will push asset prices somewhat higher, investors/savers will still want to save, lenders will still be cautious lenders, and cautious borrowers will remain cautious, so we will still have “pushing on a string.” As a result, Monetary Policy 3 will have to be directed at spenders more than at investors/savers. In other words, it will provide money to spenders and incentives for them to spend it. Ray Dalio Bridgewater Associates

This latest rally saw investors chasing safe haven and dividend paying stocks like consumer staples and utilities. Investors are moving ahead but with caution. Other safe haven assets performed well in Q1 such as US Treasuries, Municipal bonds and Gold. We are also seeing investors maintain cash positions to levels not seen in years. We think that those are good signs. The fact that investors have sought and are seeking shelter will provide some cushion to any market tumble. Investors are preparing for another 2008 style crash. That, in essence, is why 2016 is NOT 2008.

Clients have been asking what metrics we are looking at as far as taking more equity risk. The 200 Day Moving Average (DMA) is the Maginot Line when it comes to seeing markets as bull markets or bear markets. Obviously, we would take more equity risk if we felt that we are in a bull market. Currently with the S&P 500 in a battle to take flight above its 200 DMA we are inclined to believe that we are still in a bear market and continue to hedge risk. If the bulls can get above and stay above the 200 DMA in the S&P 500 we would be more inclined to changing our mindset.

Oil’s bounce is alleviating pressure on borrowers and drillers but prices need to get back above $50 a barrel to really stop the pain. Currently, as we write West Texas Crude is below $40 a barrel. The selling of oil and oil related debt may be easing for now but the pain may only be delayed. High yield debt has seen money pour into that sector in the last month. Investors may be catching a falling knife there with more pain to come if oil cannot continue its recent rally.

We will continue to tactically change our asset allocation as the S&P 500 stays range bound between 1800-2100 and volatility continues its resurgence in 2016. We continue to hold bonds as it has been the most unloved of asset classes for the last several years as short sellers have been betting on rising interest rates and falling bond prices. In Q1 of 2016 bond returns have been in excess of 2% which is a very nice quarter for bonds. We see bonds as having value while the US 10 year yield is still north of 1.8% as we write while Japanese 10 year rates are less than zero. We feel that there is still adequate return to entice capital from around the world into US government bonds at 180 basis point spreads.

We cannot predict with 100% accuracy every move in the market but what we can do is try and profit by tactically allocating and hedging our portfolio in times of market stress to take advantage of market volatility. Investing is not a game of perfection but of managing the risk inside one’s portfolio. We do not jump in and jump out of the market wholesale. By divesting ourselves of overpriced assets and availing ourselves of opportunities when prices are low allows us to take advantage of the long term benefits that the math of compounding brings.

We still foresee 2016 as being a tactically driven year. We feel that changing our positions tactically with the ebb and flow of the market, decreasing the volatility of our portfolios by increasing positions in bonds and bond like instruments while also paying attention to companies that have pricing power like technology and health care will be the key to performance. Cash is also an important part of asset allocation because although it returns zero when risk premiums rise its value will be seen in its inherent call optionality and the opportunity set that it provides given lower asset prices.

I think we aspire less to foresee the future and more to be a great contingency planner… you can respond very fast to what’s happening because you thought through all the possibilities, – Lloyd Blankfein CEO of Goldman Sachs